Understanding state’s estate tax farm deduction

2026March 2026

By Norman Brock

Attorney at Law, Brock Law Firm

The difficulty in writing this article and trying to explain the requirements for qualifying for the Washington Estate Tax Farm Deduction as it applies to you is that virtually every farmer or rancher estate and their operation is different than their neighbor. Just being a farmer or rancher is not enough to meet the complex rules associated with the farm deduction. Your estate must meet very specific conditions when you die, and in many instances, your estate may very well not end up qualifying for the farm deduction.

I remember (seems like yesterday) being 11 or 12 years old, selling my bunches of raised green onions for $.03 to the local grocer, or walking the neighborhood and hocking them for $.05 a bunch. I remember telling grandma I wanted to be a millionaire (not understanding, of course, what a millionaire really was).

Now, 70 years later, we add up what we have and being a millionaire isn’t a very high threshold! In fact, most clients with even a $3 to $5 million estate do not classify themselves as “rich” at all. They worry about 10 years in assisted living at a cost of $10,000-$15,000 per month. Yet our legislature says you ARE RICH if you have over $3 million net worth ($6 million for a married couple with proper planning)!

(As an aside, for a couple, the goal between you is to keep the surviving spouse’s estate at or under $3 million in nonqualifying, agricultural-based assets as will be explained and an equal or greater value of qualifying agricultural-based assets that qualify for the farm deduction.)

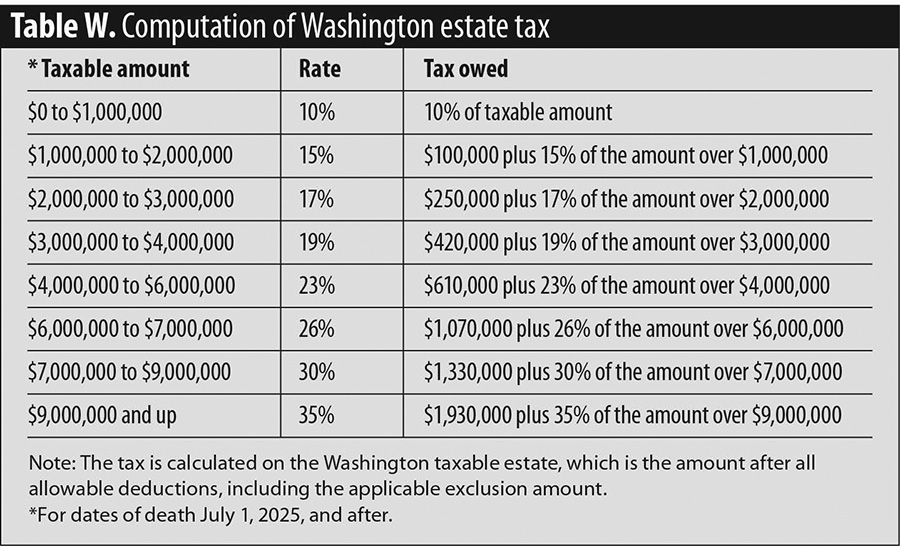

Table W is the rate chart for Washington Estate Tax as of early January.

Specifically, a farmer/rancher will need to have the following requirements for their estate to qualify for the farm deduction:

- The farm property must pass to a qualified heir from the decedent.

- The farm property must have been used for a qualifying use (farm property used for a farming purpose) for five out of the eight years prior to the decedent’s death by the decedent or a member of the decedent’s family.

- The decedent or a member of the decedent’s family must be using the farm property for a farm use on the date of the decedent’s death.

- The farm assets must make up at least 50% of the total estate’s adjusted gross value.

- The farm real property must make up at least 25% of the total estate’s adjusted gross value, which is the total gross less any mortgages or indebtedness on such farm property.

Now, say you when you die you own $10 million of assets. Applying the above conditions, $8 million of those assets qualifies as “property used for farming/ranching.” That leaves $2 million of nonfarm assets, reduced by the $3 million statutory exemption, resulting in $0 estate tax being owed by your estate after your death.

But, fail the qualifying conditions tests — which are very strictly applied — and your estate under the above scenario suddenly owes tax on $7 million ($10 million less the $3 million statutory exemption), and your estate must pay $1,330,000 to the governor!

Our office has extensive experience in dealing with the Washington State Department of Revenue (Revenue) with respect to the ag deduction and the many nuances presented by some estates trying to qualify for the farm deduction.

The following is an overview of what we find Revenue typically requires each estate must furnish (when claiming the farm deduction on the Washington Estate Tax Return):

- Appraisals of all assets— farm, vehicles, equipment, cattle, residences.

- Breakdown of all assets within a closely held entity.

- If held in an entity, the business appraisal is necessary to determine the value of the business and substantiation for any discounts applied to the entity value.

- Determination of what assets qualify for the farm deduction, and why they qualify.

- Statements of all bank accounts in the month of death to prove nonfarm asset values.

- Documentation, including leases, to substantiate the predeath, material-participation requirements imposed on the decedent and/or their family member.

Then, debt must be applied to the percentage test equation:

- Each asset must be closely identified on any debt that may be securing it.

- Does the debt result in disqualifying the estate for the farm deduction by tilting the farm assets less than the nonfarm assets for the percentage tests?

Note: Revenue presently allows a married decedent to utilize the community property interest value of farm real property owned by the surviving spouse for the sole purpose of determining whether the estate meets the farm deduction percentage test.

Pitfalls that our office has come across when representing an estate that attempts to qualify for the farm deduction include:

- Leasing part of the farm out to a neighbor for a specialty crop, such as irrigated wheat or potato crops. That land then fails to meet the rules.

- Farmer Ted goes into the nursing home a month before his death and prior to going into the nursing home, leases out the farm to the neighbor. Fail!

- Leasing the pasture land out to the neighbor who runs cattle, while the decedent owns no cattle. Fail!

- Growing potatoes in year one, but leasing out the land for wheat or alfalfa in years two and three and dying in year two or three. Fail!

- Failure to materially participate for five out of eight years prior to your death on the land, meaning it now doesn’t qualify for the farm deduction. Fail!

- The very interesting situation of a husband and wife married for 50 years. Husband’s brother is farming the land for 10 years prior to husband’s death after husband retired from farming. Husband dies first. Wife inherits the farm after death of husband and continues to lease the farm to brother of deceased husband. Brother of her husband is NOT a family member of wife according to Revenue’s definition, and wife doesn’t meet the farm deduction rules when she dies. Fail!

The opinions in this article are for general information and not intended to provide specific advice. This information is not intended to be a substitute for specific individualized tax or legal advice. The author suggests that you discuss your specific situation with a qualified tax or legal advisor.

Norm Brock has been representing farm families throughout Eastern Washington, Idaho, and Northwestern Oregon for more than 50 years. He works out of the firm’s Davenport and Spokane offices and can be reached at (509) 721-0392 or brocklf.com.